Moving home

Understanding the Mansion Tax

December 2025 | By Rob Owens

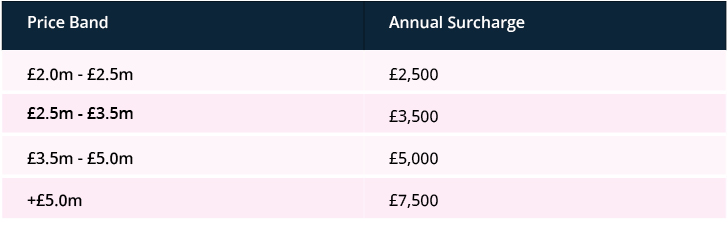

The Autumn Budget introduced a new “High Value Council Tax Surcharge”, commonly referred to as the “mansion tax”. From April 2028, owners of homes in England valued above £2 million will pay an annual levy ranging from £2,500 to £7,500, depending on property value bands.

e.surv estimates around 110,000 homes currently exceed the £2m threshold, representing less than 0.5% of England’s housing stock, with 90% of these homes in London and the South East. Our estimates also include property types beyond the stereotypical detached mansion, such as terraces and flats.

Using OBR house price forecasts to project house prices over time shows that more homes could be drawn into the tax over time, though outcomes will depend heavily on market performance.

For lenders, this policy introduces new considerations for high-value lending, borrower liquidity, and potential behavioural shifts in the prime residential market.

The surcharge applies to homes in England worth over £2 million, and is grouped into four bands:

The tax will be collected alongside council tax but paid to central government. Uprating by CPI begins in 2029. The government expects to raise around £400m annually by 2029–30.

Council-owned homes are exempt from the surcharge. There has yet to be a similar exemption for socially rented homes owned by housing associations.

For individuals unable to pay, the policy includes a deferral mechanism, that allows the charge to roll up and be settled upon the sale or transfer of the property. This aims to protect asset-rich but cash-poor homeowners.

What remains unclear is the valuation process: a nationwide revaluation is scheduled for 2026 but appeals and disputes are likely. There is also uncertainty around whether the CPI adjustments will be applied to property prices or only to the annual surcharge.

Key Findings

Using e.surv’s AVM to approximate the value of the 27 million homes in England, we estimate 110,000 properties currently exceed the £2m threshold in 2025.

Regional split Around 90% of homes over £2m are located in London (66.4%) and the South East (22.4%)

Local authority hotspots Homes in Kensington & Chelsea and Westminster account for 25% of the stock liable for the surcharge. This equates to 21% and 13% of all homes in K&C and Westminster, respectively.

Property types Detached houses make up nearly half (48%) of the affected homes, but terraces (24%) and flats (15%) also represent a significant share – perhaps challenging the perception of what a “mansion” might be.

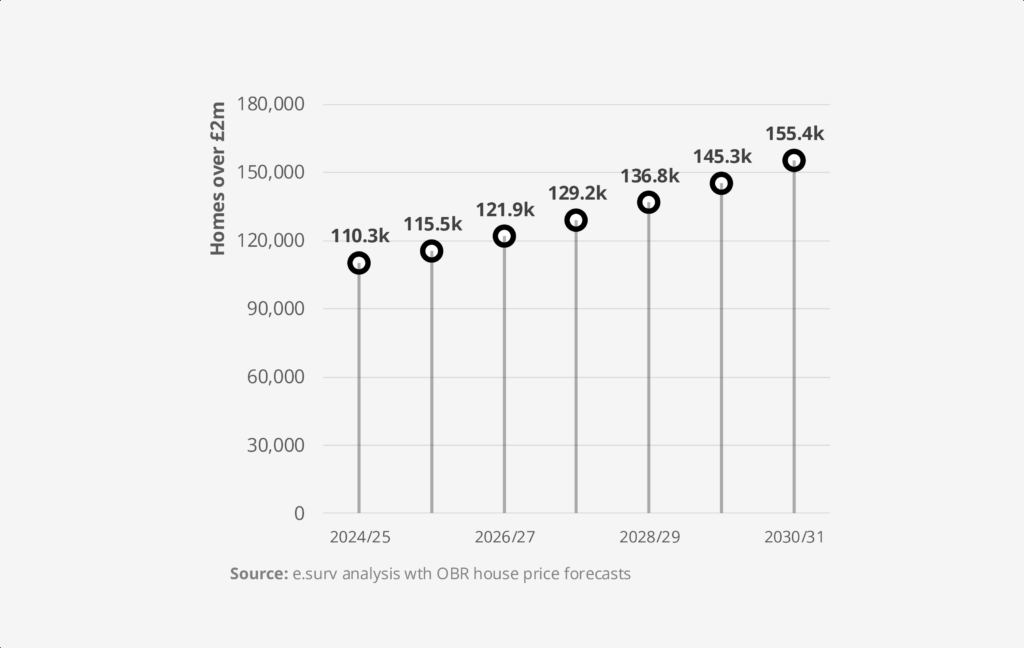

Long-term impact Based on OBR’s house price forecasts, an estimated 45,500 additional homes will cross the £2m threshold by 2030/31 – a 41% increase on today’s total

Using e.surv’s AVM to approximate the value of the 27 million homes in England, we estimate 110,000 properties currently exceed the £2m threshold in 2025.

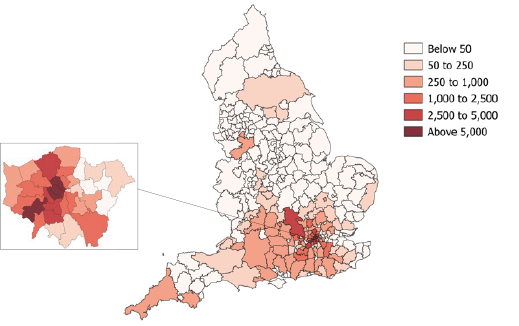

The heat map shows where homes currently liable for the mansion tax are concentrated.

London and the South East dominate, accounting for around 90% of eligible properties. Kensington & Chelsea and Westminster alone make up 25% of the total, with 21% and 13% of all homes in those boroughs above £2m.

Outside these regions, exposure is limited but notable in Trafford, Cheshire East (around 500 homes each), and areas such as Birmingham, Warwick and Northumberland.

Applying the OBR’s house price index forecasts to 2030/31, we project a gradual increase in the number of homes crossing the £2m threshold. Under baseline assumptions, the figure could rise from 111,000 today to circa 155,000 by 2030/31, an uplift of 41%.

However, this projection assumes uniform growth across all price segments and regions, which is unlikely for prime residential markets. The next slides looks to explore

price sensitivity.

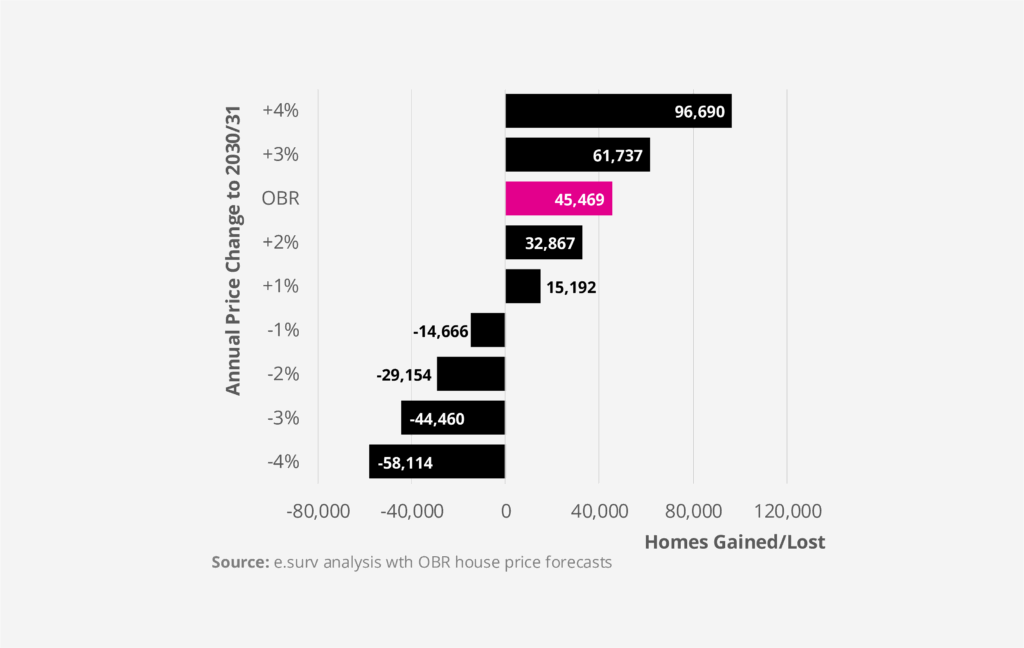

To illustrate sensitivity, we tested scenarios from -4%to +4% pa from 2025/26 to show the number

of a homes that would be dragged into (or out of) the £2m+ threshold by 2030/31.

This divergence highlights a key risk: the mansion tax could create a two-tier market, with properties clustering just below £2m to avoid the surcharge. Liquidity at the top end may decline, and asset-rich, cash-poor owners could face unintended affordability pressures, prompting downsizing or inheritance tax challenges later on if payment of the surcharge is deferred by the homeowner.

Shift in Property Taxation

Mansion tax marks a move toward taxing property wealth, not just transactions.

Uncertainty of Impact

Exposure could rise 50% or fall under stress.

Regional Concentration

90% of affected homes are in London and South East – regional risk matters.

Valuation Challenges

While AVMs are likely to play a part in identifying the stock of homes, model performance in areas where high-value homes are less common may prove challenging

Market Behaviour Risks

Expect price clustering below £2m, slowing transactions and creating valuation challenges.

Opportunities for Lenders

Downsizing and advisory services create remortgage and client engagement opportunities.